Why Spring 2026 Is a Genuine Inflection Point

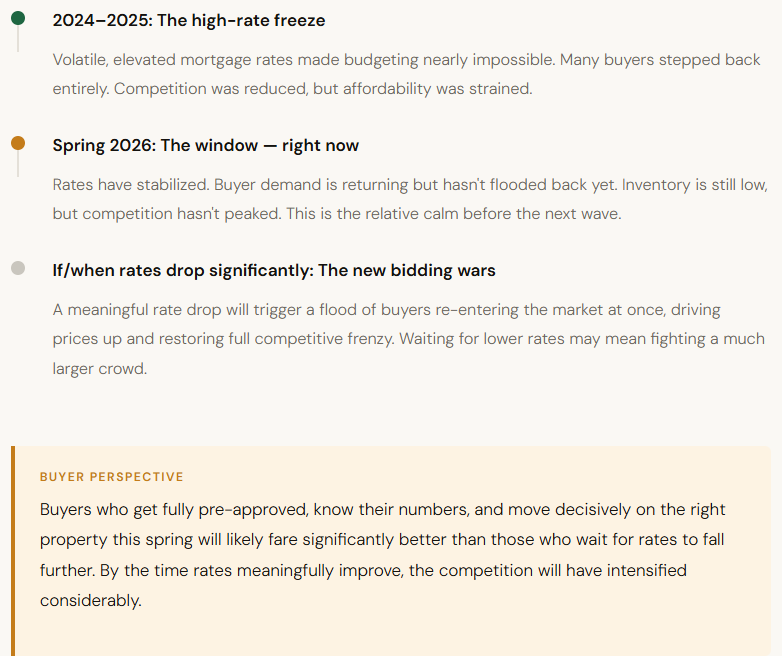

The past two years were defined by elevated mortgage rates and cautious consumer sentiment that kept much of the market frozen. Sellers didn't want to give up their low-rate loans. Buyers couldn't stretch their budgets far enough. The result: low transaction volume on both sides.

That dynamic is shifting. Rates have started to stabilize, buyer confidence is recovering, and years of pent-up demand are beginning to unlock. The combination creates both urgency and opportunity — but the window is specific, and knowing how to act within it depends on which side of the transaction you're on.

For Sellers: Low Inventory Is Your Competitive Advantage

The most defining characteristic of the spring 2026 market for sellers is simple: there aren't enough homes for sale to meet demand. That supply-demand imbalance works directly in your favor — when buyers have fewer options to compare, well-priced and well-presented properties attract serious attention quickly.

In many markets, multiple-offer situations are returning. This isn't the peak frenzy of 2021, but conditions are favorable enough that sellers who approach the market thoughtfully are seeing strong outcomes.

The one trap to avoid: overpricing

After two years of rate sensitivity, today's buyers are financially aware and cautious. Homes priced above market value are sitting longer and — critically — often selling for less than they would have if priced correctly from day one. The inventory advantage only works when you meet the market where it is.

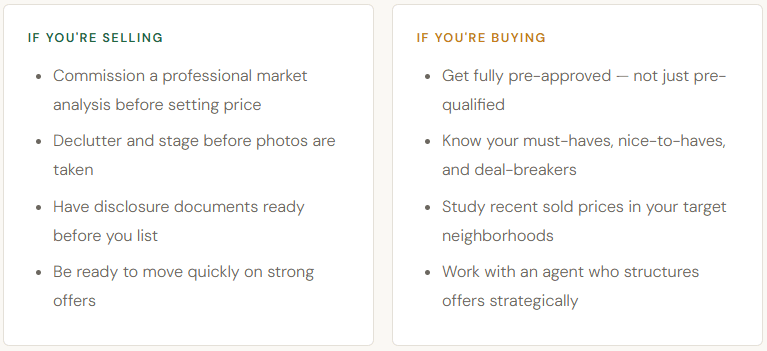

What effective spring preparation looks like

For Buyers: You're Inside a Narrow Window of Opportunity

For the past two years, elevated mortgage rates compressed purchasing power and sidelined millions of would-be buyers. That's changing — rates have plateaued and could ease further by mid-year. More importantly, their stabilization makes monthly payments predictable again, which gives buyers the confidence to commit.

Here's the strategic reality: you are currently sitting between two difficult market conditions.

Acting decisively doesn't mean acting recklessly

Urgency and discipline aren't mutually exclusive. Know your budget ceiling before you tour a single home. Understand what comparable properties have actually sold for — not just what they're listed at. Don't waive protections you can't afford to lose. Have an agent who knows how to structure a competitive offer, not just how to submit one.

For Everyone: Preparation Is the Real Competitive Edge

Whether you're buying or selling, the single theme that runs through this spring market is consistent: preparation separates the people who succeed from those who end up frustrated.

Frequently Asked Questions

Is spring 2026 a good time to sell a house?

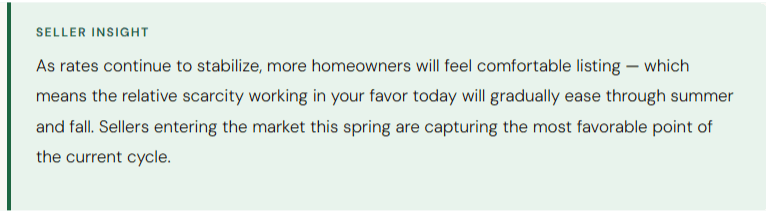

Yes — for most sellers, spring 2026 offers a meaningful strategic advantage. Inventory remains historically low, meaning well-priced homes attract serious attention and multiple-offer situations are returning in many markets. That said, the window is narrowing: as rates stabilize and more homeowners feel comfortable listing, supply will grow through summer and fall. Acting this spring captures the most favorable point in the current cycle.

Should I buy a house now or wait for mortgage rates to drop?

Waiting for a significant rate drop may backfire. When rates fall meaningfully, a wave of sidelined buyers will re-enter the market simultaneously, driving prices up and intensifying competition. Spring 2026 is a relative window of calm before that flood. Buyers who are pre-approved and ready to act now are likely to face less competition — and potentially more leverage — than those who wait.

Why is housing inventory still so low in spring 2026?

Low inventory is largely a legacy of the elevated mortgage rate environment from 2024–2025, which kept many homeowners locked into low-rate loans they were reluctant to trade in. As rates stabilize, some of that supply is beginning to return — but gradually. For now, the imbalance between supply and demand continues to favor sellers in most markets.

What is the rate lock-in effect, and is it still relevant?

The rate lock-in effect describes homeowners who won't sell because doing so would require them to give up a low mortgage rate secured in prior years and take on a higher-rate loan. This has been a major driver of low inventory since 2023. As current rates stabilize and the gap between existing and new mortgages narrows, more sellers are gradually becoming willing to move — which will slowly rebuild inventory through 2026.

How do I prepare to compete in a spring 2026 bidding situation?

Start with a full mortgage pre-approval — not a pre-qualification. Know your priorities clearly before you tour homes. Work with an agent who understands how to structure competitive offers using tools like escalation clauses, flexible closing timelines, and earnest money strategy. And study recent sold prices so you can move confidently and quickly when the right property appears.

Get a Personalized Market Analysis

Every neighborhood moves differently. Find out exactly where your local market stands — and what your best move looks like this spring.

Request Your Free Analysis

Categories

Recent Posts